Creative services such as advertising, publishing, and design are an important part of global trade. Their rise has been partly due to technology, which has made it easier to trade intangibles, but also because of increasing integration into the production of manufactured goods. In the decade before the pandemic, cross-border trade in services increased 60% faster than trade in goods.

In a new AHRC-funded Creative PEC project, published in Regional Studies, we are using data from the Inquiry in International Trade in Services (ITIS), in combination with the Annual Business Survey (ABS), to provide new evidence on the scale, trends, and geography of UK creative service exports. Second, we develop a measure of industrial relatedness between exports of creative, non-creative services and manufacturing goods to investigate the frequency with which they co-locate with other parts of the economy.

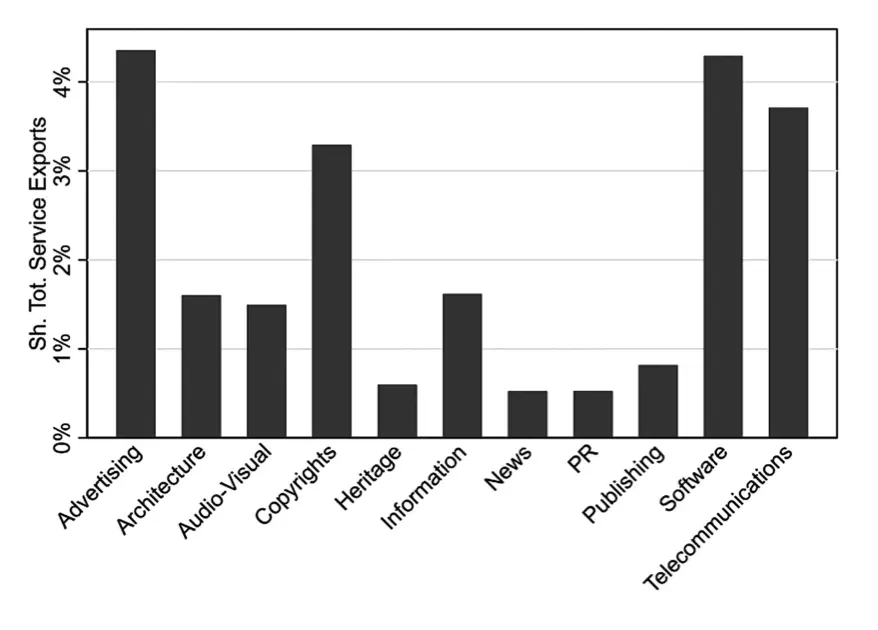

Creative services are a diverse group. The largest part of service exports come from Software, Telecoms, Advertising and Copyrights (copyrighted literary works, sound recordings, films, television programmes and databases). Together these account for around 15% of total UK service exports. As figure 1 shows, other services such as architecture, audio-visual and information also play a role.

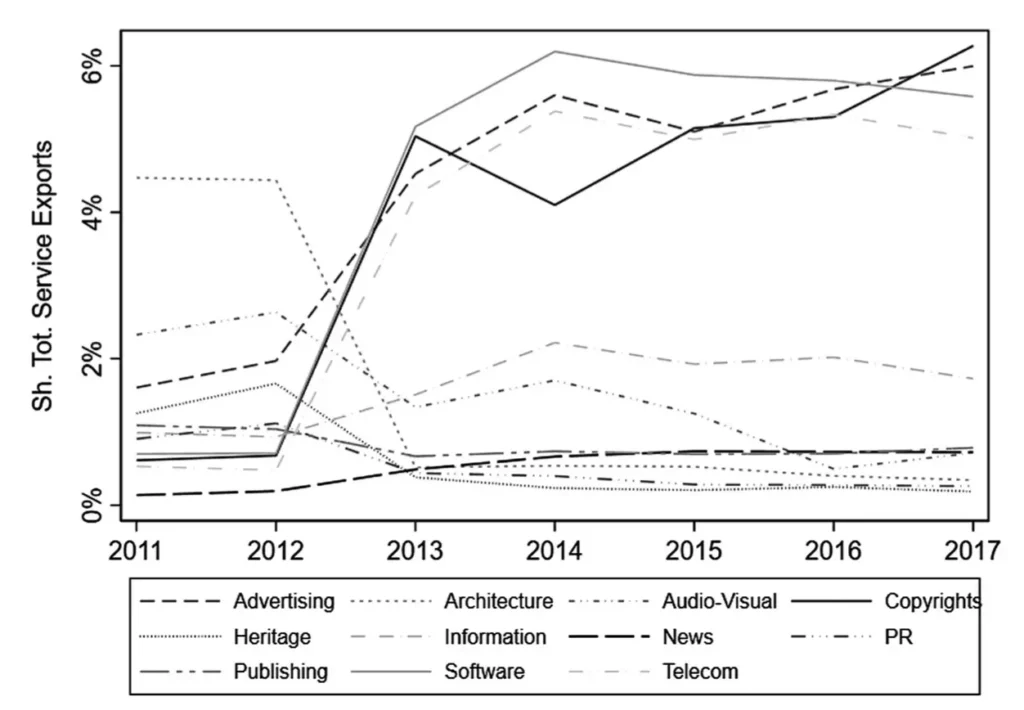

There has been considerable change in the export propensity of these sectors over time. Exports of advertising services, copyrighted creative works, telecommunication services, and computer software have been particularly important, accounting for around 5% of total services exports each. There has been a rapid increase in the share of services in four of the sectors which form the top 10: copyrights, advertising, software and telecommunications, while a relative decline in the share of architectural and audio-visual services exports.

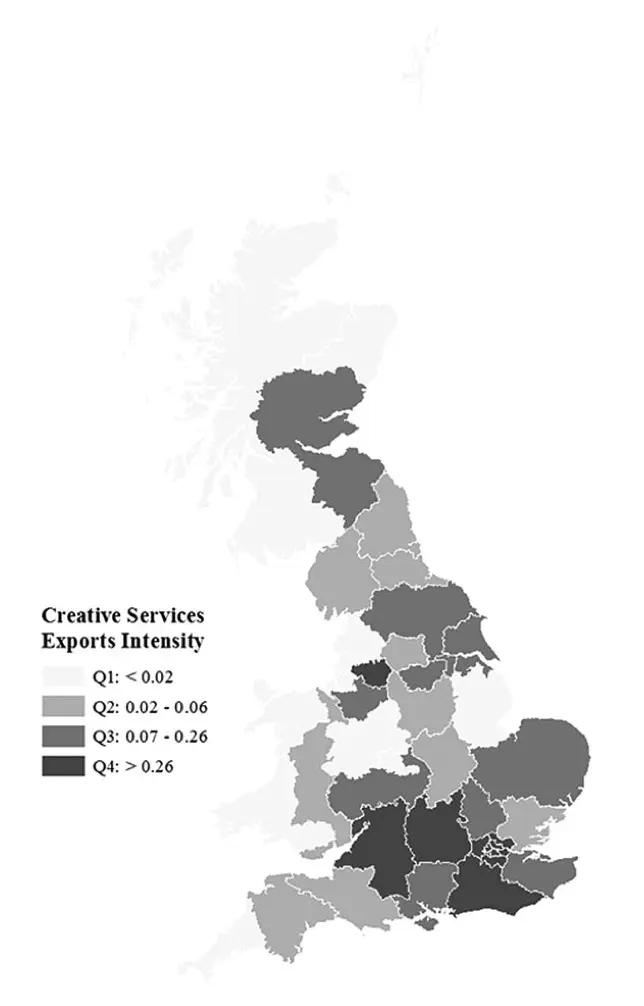

Creative service exports are highly geographically clustered, particularly in London and the South-East, Oxfordshire, Greater Manchester and Yorkshire. This partially reflects the geographical distribution of creative industries. The South-East and London account for around 40% of creative industry employees and a third of creative businesses, so it is hardly surprising that this is where most creative service exports come from.

Where do these exports go?

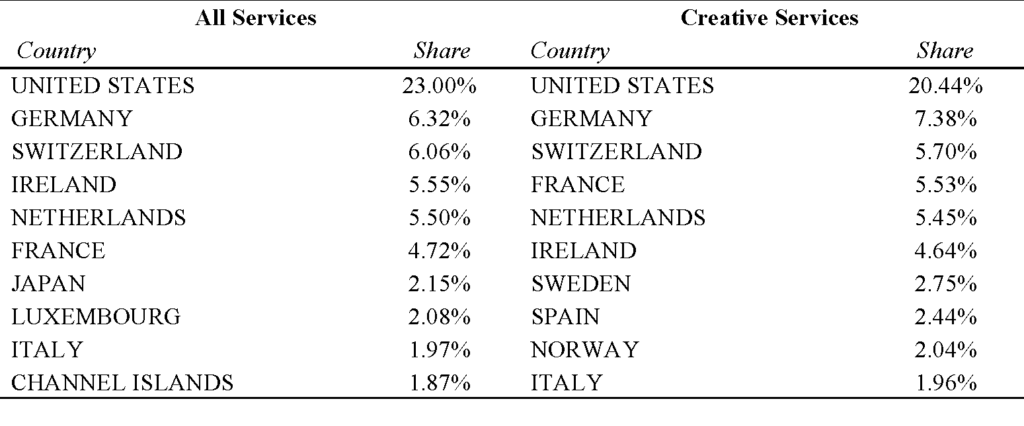

The largest share of UK creative service exports go to the United States, with over a fifth heading there. Germany, France and other EU countries are also well represented – although there is also considerable trade with Switzerland and Norway. Our data only goes to 2017, so won’t have accounted for the impact of Brexit – but they do show a problem for UK policymakers with EU (and EU linked) destinations so important.

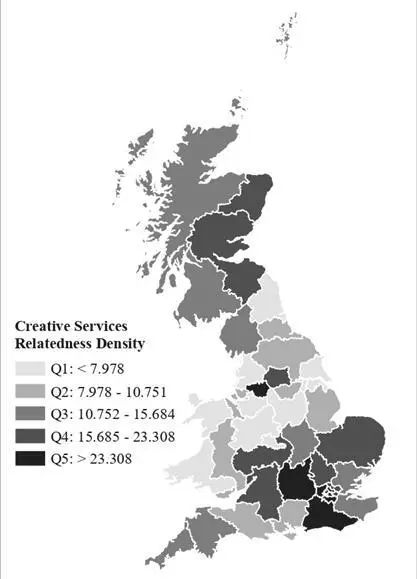

Future Creative Service Growth

We also show relatedness between creative services exports and the rest of local industrial structure in figure 4, above. This shows the type of environments which might be suitable for future creative service growth, and the type of industries with which they tend to co-locate (potentially giving information on local input-output links). Creative service exports are particularly well suited to urban areas (London, Manchester, Edinburgh, Leeds) and hubs of knowledge creation (East Anglia, Oxfordshire, Surrey, Sussex and Warwickshire). These are places where clusters of universities and knowledge intensive industries could play a key role in fostering the growth of creative services.

Existing comparative advantage in manufacturing and other services exports could allow regions to diversify away from mature industries and specialize in new creative services.

Creative services have become increasingly important part of international trade. Future developments in ICT and innovation in digital services are likely to make the sector even more important in the future. As a key strength of the British economy, laying the conditions for creative services to continue their export success will be an important part of any future UK growth strategy. If the UK is to succeed as a trading nation, creative service exports will need to play an important role.

__________________________________________

Thumbnail image by Lars Kienle on Unsplash

Hero image by Mario Caruso on Unsplash

Related Blogs

Measure what matters: Priority pathways and Creative Higher Education

Bernard Hay, Creative PEC's Policy Director, investigates the surprising absence of creative subject…

11 actions for the cultural and creative industries in the age of AI

A guide to help the cultural and creative industries address the rise of AI, from the GCEC.

Creative Resilience in Times of Crisis

Introducing A Global Agenda for Creative Resilience, an 11-point strategic framework for strengtheni…

Reporting from the Creative PEC Research Symposium 2026

Bringing people together from across academia, industry, and government for discussion and debate on…

Keeping creative options open for everyone

How does creative study allow us to express ideas, shape how we see the world, and contribute to vib…

Coworking spaces as informal skill ecosystems for the creative workforce

How coworking spaces have become an increasingly important component of the creative economy.

From Wales to the World: Why International Cultural Policy Needs a Future Generations Lens

Can international cultural policy be shaped by focusing on future generations?

10 facts about Creative Industries growth potential

Discover ten key findings from the report 'High-Growth Potential Firms in the UK's Creative Industri…

Why London is investing in Creative Enterprise Zones

London Mayor Sir Sadiq Khan announces £2.2 million in new funding for Creative Enterprise Zones.

Research resources on Creative Clusters

We’ve collated recent Creative PEC reports to help with the preparation of your Creative Cluster bid…

What UK Job Postings Reveal About the Changing Demand for Creativity Skills in the Age of Generative AI

The emergence of AI promises faster economic growth, but also raises concerns about labour market di…

Creative PEC’s digest of the 2025 Autumn Budget

Creative PEC's Policy Unit digests the Government’s 2025 Budget and its impact on the UK’s creative …